Maintaining a stable investment course for the months ahead.

With files from Manulife Investment Management Co-Chief Investment Strategists Kevin Headland and Macan Nia.

As we round out the end of 2021, markets continue their push for new all-time highs, there are fewer pandemic restrictions affecting businesses and consumers, and cross-border travel between Canada and the U.S. is on the upswing. But at the same time, inflation, supply chain disruptions, and labour challenges are on the minds of many, heightening the potential impact it may have for investors heading into 2022.

To help make sense of it all, Kevin Headland and Macan Nia, Co-Chief Investment Strategists with Manulife Investment Management, offer their views on inflation, rate hikes, portfolio re-balancing, and more, beginning with a look at the consequences of a slowing economy.

Economic strength

“We’re seeing a general economic slowdown that is happening right across the world, and a term starting to creep into the lexicon more and more is stagflation,” says Kevin. “This can be defined as an environment where inflation is increasing but economic activity is decreasing.”

But is stagflation the right term? Macan Nia suggests otherwise.

“I wouldn’t say we are in a stagflation environment, but rather a slowflation environment,” says Macan. “Yes, inflation is increasing, but economic activity is not decreasing at a rate where we feel concerned. There is a slowdown from peak summer levels, but things are still looking good for earnings and positive market momentum.”

There are, however, notable concerns about a slowing economy in China, with weaker copper prices supporting this narrative. Copper prices are dropping, which can be seen as the result of a decrease in manufacturing demand.

Copper prices are signalling a slowing Chinese economy

Chinese Imports vs Copper Prices YOY Change 2006-Current (with 6-month forward forecast)

Source: Capital Markets Strategy, Bloomberg. As of September 30, 2021

It’s interesting to note that some of this economic weakness may be voluntary. “An example of this self-induced weakness is with emission rates, where China wasn’t on track to meet emission targets,” says Macan. “As a result, factories that rely on coal were ordered into rolling shutdowns, impacting economic activity.”

Along with emission rates, China appears to be having difficulty importing coal from Australia and Mongolia. And one of China’s major coal-producing areas has also been heavily affected by recent flooding.

Looking ahead, the Capital Markets Strategy team feels the current weakness in the Chinese economy is likely to be short in nature, with the government stepping in and allowing factories to resume production at full capacity, thus resuming an upward trend heading into 2022.

Inflation and investments

There are a variety of adjectives to describe inflation: transitory, persistent, enduring. But rather than focusing on a word to describe inflation, the focus should be on where it will end up. Will inflation stay in the five per cent range? The Capital Markets Strategy team is doubtful.

“Inflation has likely been more persistent than many investors and the central banks expected, with supply chain interruptions and the pandemic also more persistent than expected. But if we look ahead two years, we fully expect inflation to be more in the range of 2 per cent,” says Macan.

Even so, the effect of inflation on investment returns can’t be ignored.

“Imagine a retiree on a fixed income. If they aren’t earning more than inflation on their investments, they’re losing money. The cost of goods goes up more than their return on their investments, eroding their savings. We need to be cognizant of that,” says Kevin.

Currently, U.S. 10-year Treasury bonds are delivering returns in the range of 1.5 per cent. To compensate for inflation, the 10-year needs to be trending higher.

“Real yield also needs to be considered, and this is simply the rate of return on a bond minus the rate of inflation. If a bond is earning 2.5 per cent and inflation is 2 per cent, then the real yield is 0.5 per cent. So, when we consider inflation higher than 2 per cent, the yield on a 10-year U.S. Treasury bond should be in the range of 2.26 per cent, based on the long-term average real yield, to compensate for inflation,” says Kevin.

All this is to say, the Capital Markets Strategy team feels the trend will be higher U.S. 10-year Treasury yields and higher rates for Canadian long-term bonds to compensate for higher inflation — above 2 per cent.

Portfolio balancing act

The Capital Markets Strategy team continues to be optimistic heading into 2022 but cautions that a new approach is needed for the stabilizing portion of an investment portfolio.

“For a few years now, we’ve fielded questions on whether the 60/40 portfolio is still relevant, and I enthusiastically say, yes,” says Kevin. “However, the 40 per cent allocation to fixed income needs to be re-imagined. There’s a need to be flexible and look at all the different types of bonds that can generate returns and offer downside protection for this new environment that we’re in.”

“In September’s market pullback, we experienced our first monthly loss with the 60 per cent equities/40 per cent bonds portfolio for 2021,” says Macan. “Typically, when equities experience a pullback, bond rates rise to act as a stabilizer, but we didn’t see that in September.”

Moving forward in a rising inflation environment, the fixed-income portion of portfolios will be challenged, but there are ways to mitigate the downside. Strategies can include decreasing the duration of the fixed-income portfolio, increasing the percentage of high-yield bonds, and considering a wider global scope that swaps out some of the Canadian sovereign bonds with emerging market opportunities.

“For a long time, Canadian investors rarely had access to global securities, and we now have a bigger sandbox to play in,” adds Kevin. “You want to be able to invest anywhere in the world. Investors have embraced this mindset for equities, and slowly this thinking is shifting for fixed income. The reality is that the global fixed-income market is larger than the global equity market. There are a lot of opportunities out there for fixed income, you just need to be open to the idea of moving beyond traditional fixed income vehicles.”

Navigating a market pullback

In the event of a market sell-off, is there a secret formula? By analyzing the data for the S&P 500 index back to 1970, during environments that are positive and recessionary, the Capital Markets Strategy team finds that market selloffs indicate a time to buy.

Investors are rewarded by buying when the market sells off

S&P 500 Price Index 1-year forward returns after selloffs from 52-week peak (1970 – current)

Source: Capital Markets Strategy, Bloomberg. As of September 30, 2021

“This is a completely normal playbook coming out of a recession. There are three phases to a bear market and recovery, and we are now in the third phase, which is the normalization period,” says Kevin. “Do we think we will see 20 per cent returns in equities over the next 12 months? Probably not. Do we think equities will outperform fixed income? Very likely. That’s why we have not made any changes to our model portfolio, which is 65 per cent equities to 35 per cent fixed income.”

Source: Capital Markets Strategy, Bloomberg. As of September 30, 2021

“Within fixed income, navigating a rising rate environment requires being open to shorter duration bonds and higher yield bonds to mitigate potential downside,” says Macan.

If and when there’s a pullback, there’s an opportunity to increase a portfolio’s investment weight in equities or use cash on the side to get into equities. But the Capital Markets Strategy team cautions that expectations for returns over the next 12 months need to be adjusted.

Credit and rate hikes

Along with rising inflation, there may be concerns that the cost of borrowing will also increase, which has the potential to curb consumer spending. But is this an immediate cause for concern? The Capital Markets Strategy team feels that consumer confidence is a reason for optimism.

“It is our team’s view that rates are likely to increase, and there is concern that rising interest rates may impact consumer spending and borrowing. However, there are good indicators that consumer confidence is steady,” says Macan.

“Numerous banks have recently reported that their loan growth is improving. As consumers begin to have more confidence in their environment, in their jobs, they are more comfortable with the idea of taking on additional debt — a sign that the economy is improving,” say Kevin. “There are also indicators that credit card debt is increasing, which is a positive sentiment that the consumer is feeling confident enough to begin spending again.”

When considering rate hikes, the U.S. Federal Reserve relies on data such as the Chicago Fed National Financial Condition Credit Subindex, among others, to determine the right course of action. At present, the Capital Markets Strategy team agrees that credit conditions continue to be quite good, maybe not as favourable as 2020, but with no significant reason for concern.

The Fed has kept credit conditions very accommodative

Chicago Federal Reserve National Financial Conditions Credit Sub-Index (1971 – current)

Source: Capital Markets Strategy, Bloomberg. As of September 30, 2021

“We don’t expect a rate increase from the Federal Reserve in the near future, but we do think the Fed will begin to taper asset purchases. When the Fed does begin to reduce monthly asset purchases, it will reduce some of the liquidity in the marketplace, tightening credit conditions. But we don’t feel like it will create a situation where there isn’t enough liquidity,” says Kevin.

From a corporate perspective, there’s still good support from the fixed-income sector for companies that want to raise capital. Bank earnings are also strong — another solid indicator of economic confidence.

“When looking for recession indicators, one sign is that credit conditions become tighter. In our current environment, where credit conditions are quite accommodating, we feel the risk for recession is quite low,” says Macan.

Real estate

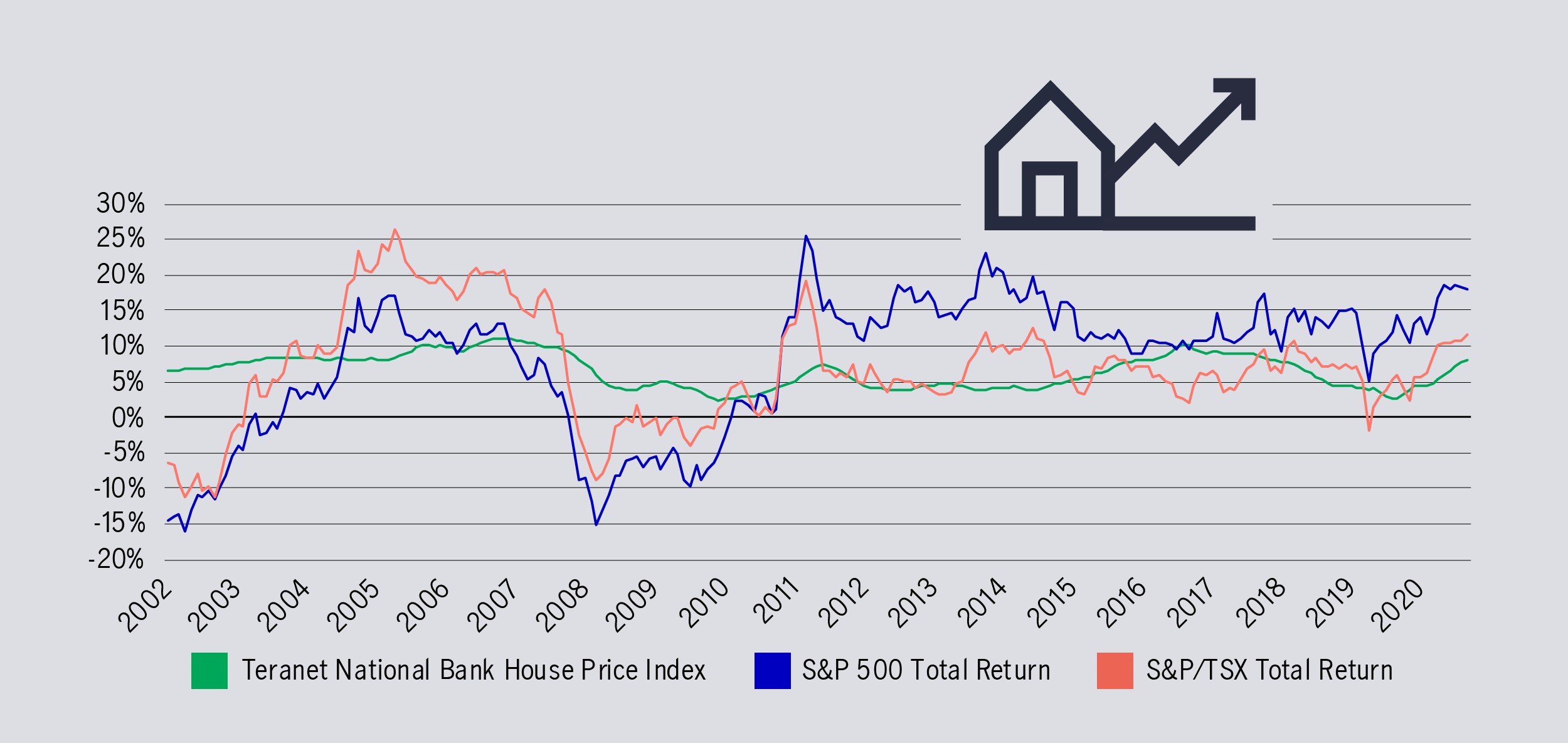

As housing prices skyrocket across Canada, there can be a tendency to think that real estate may be the stronger investment opportunity. But for those investors who wonder why they should stay invested in the stock market versus investing in real estate, the research is eye-opening.

“We went back to 2002 and compared the S&P 500 Total Return Index and then S&P/TSX Total Return Index with the Teranet-National Bank House Price Index. Using a three-year rolling return, the returns in the equity markets are better, but they come with more volatility, ranging from -15 per cent during the lows of the 2008 financial crisis to 25 per cent in 2012, and then averaging in the 10 to 15 per cent range during the past five years. When you look at the Teranet House Price Index, on a rolling basis, the average is about eight per cent during the past five years,” says Macan.

Equities tend to outperform Canadian home prices but are more volatile

Teranet National Bank House Price Index vs. S&P 500 and S&P/TSX Total Return Index 3 Year Rolling Returns (2000 – current)

Source: Capital Markets Strategy, National Bank, Bloomberg. As of August 31, 2021

When you look at the history of equities, they have done just as well, if not better, over the long term, as compared to Canadian house prices.

“When house prices are up 20 per cent, it can be easy to get caught up in the thinking that they will go up 20 per cent every year, but that’s just not the case. And when you look at the historical data, there are times where house prices are very stagnant and don’t move for nearly a decade,” says Kevin.

The advantage of being invested in equities is the exposure to risk. Portfolios can be adjusted to accommodate for growth areas of the market and protection against downside risk. This kind of opportunity doesn’t really exist with real estate.

“The reality with real estate, as well, is the amount of leverage required — investors need access to the funds for a down payment to get into real estate, whereas it’s not the same situation for investing in equities,” says Macan.

While there’s no shortage of alarming headlines that can generate pessimism, such as pandemic variants, peak growth, debt ceilings, and manufacturing slowdowns, it’s also important to note that economic growth is in a good position.

“We were experiencing levels of growth that would be unsustainable over the long term. Now we are growing at a pace that is very positive for employment, housing, and earnings, and that is constructive for equities looking out on a one-year time horizon,” says Macan.

“Yes, things are slowing, but things are still good. There’s no reason to be fearful of this environment over the next year,” says Kevin.

For more insights from Manulife’s Capital Markets Strategy team, check out the Investments Unplugged podcast or visit their webpage here.