From peak rates to market bottoms, what does the rest of 2023 have in store?

Spring has sprung, and there’s a distinct feeling of change in the air. Following a volatile 2022 that featured flailing equity markets and struggling fixed income returns, we may finally be on the brink of a big change.

One by one, central banks have started to reduce the speed and size of their interest rate hikes. The Bank of Canada had paused further actions since January and the U.S. Federal Reserve (Fed) had raised the federal funds rate by only 50 basis points in 2023. Policymakers have hinted that the Fed may raise the rate by only 25 basis points in May and then be “on pause.” The markets are now pricing in the potential for three rate cuts for 2023. However, the elephant in the room is the stability of the banking system.

The closures of several U.S. regional banks in March sent a wave of panic through the financial system, and the federal government deployed measures to shore up other banks. For economists, the events were reminiscent of the sub-prime crisis of 2007–2008, when multiple banks failed and a deep recession followed.

Whether the recent bank failures are isolated incidents or signs of a systemic problem, the rapid rise in interest rates may have played a role. In one of its fastest rate hike cycles in history, the Fed raised its policy rate by 425 basis points in 2022, including four consecutive hikes of 75 basis points. The Fed’s smaller March 2023 increase may have taken bank stability into consideration, but the central bank’s main mandate remains the tough task of bringing down inflation to more familiar levels. Employment continues to be strong and wage pressures are high, contributing to sticky inflation that is hard to fight.

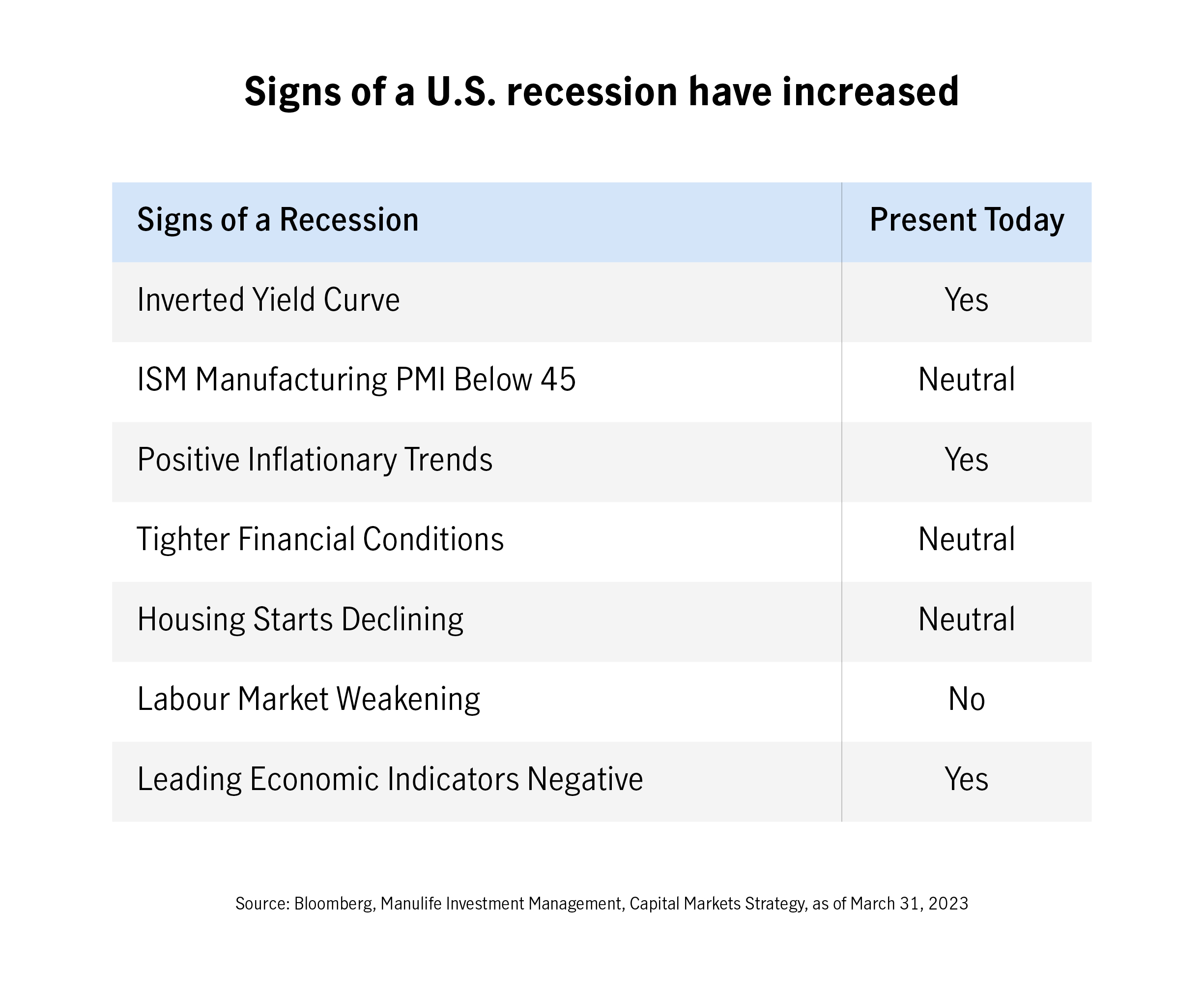

Recessionary reaction

According to the typical indicators, a recessionary environment may currently be developing, with employment being the only outlier. Time will tell whether the central banks have made the right call with their rate-setting policies, but the risk of a policy mistake can be exacerbated at inflection points like this one.

Raising rates too aggressively could cause a deep recession, while cutting rates too early or too fast could reignite inflation and force central banks to backtrack, spurring more hikes. This scenario does not appear to be unfolding, at least not in Canada, where inflation has continued to drop since the Bank of Canada paused increases.

This delicate point in time could present several opportunities for investors to put their money to work.

What the current environment says about a recession

Catching a falling knife

The possibility of a recessionary environment in the second half of 2023 could mean continued uncertainty in equity markets around the world. A prudent approach to the equity markets may be in order, and investors are right to be cautious about committing capital as they look for safety and stability. In this situation, large-cap dividend-paying equities tend to hold up better.

The response to recent volatility in the U.S. banking system may inspire other North American financial institutions to shore up reserves and curtail lending as part of an effort to stop the contagion from spreading. If that’s the case, smaller, less-capitalized companies could face difficult headwinds financing operations. Large, well-capitalized companies that are financially sound may not meet these temporary headwinds. Fed Chair Jerome Powell commented on the possible effects of tighter financing:

“Such a tightening and financial conditions would work in the same direction as rate tightening in principle. As a matter of fact, you can think of it as being the equivalent of a rate hike. Or perhaps more than that, of course, it’s not possible to make that assessment today with any precision whatsoever.”

Eventually, as the dust settles and we find ourselves in either a recession or a soft landing, mid-cap stocks might become more attractive, as they tend to do better in the two years following a market bottom. In terms of forward returns in a bear market scenario, U.S.-based mid-cap companies stand out, as seen in the chart below. This outperformance may be due to the diversity of companies that make up the mid-cap space in the United States – and the valuations. Although most stocks tend to do well in the first two years after a market bottom, mid-caps have historically outperformed in the United States.

For more insights on the U.S. mid-cap story, see Invest in tomorrow's potential household names today.

Coupon clipper

The swift rise in interest rates has made corporate high-yield bonds more attractive, but as central banks move closer to the start of a rate-cutting cycle, it could be a good time to evaluate bond holdings.

If a recession begins to materialize in the second half of 2023, then it might be time to move from “clipping the coupon” into longer-dated government debt. Historically, longer-term government bonds have fared well both leading into and during recessions as rates begin to fall. In adding duration to a bond portfolio, the decreased sensitivity to interest rate declines becomes a potential tailwind to performance. As economic conditions evolve from restrictive monetary policy to more accommodative policy, duration becomes an investor’s friend.

At the short end of the yield curve, volatility has already started. Two-year yields dropped significantly in the middle of March, in response to the banking crisis and the expectation that the Fed may start looking at cutting the federal funds rate. The main risk is the potential for a policy mistake by central banks, as discussed above.

To learn more about the outlook for bonds and the various phases of fixed income investing see Forecasting a better future for fixed income.

Is 60/40 back?

The current inflection point may very well be the moment when economic cycle fundamentals change and our old friend the 60/40 portfolio makes a comeback. Last year, rather than taking a serious look at the once-in-a-generation conditions that caused both equities and fixed income investments to lose significant value, pundits were confidently proclaiming the death of the 60/40 portfolio.

Given today’s environment, with bonds once again providing meaningful income, holding 40 per cent of a portfolio in fixed income assets may make sense. For the equity portion, a geographically diverse strategy may be beneficial as different regions tackle inflation and enter the rate-cutting stage at different times.

If we do see a market bottom and the green shoots of recovery, U.S. mid-cap stocks could perform better in this environment. If recessionary indicators continue to build and North America enters an official recession, large cap dividend paying equities may offer some shelter from the storm.

Whether it leads to a recession or the often talked about and rarely seen “soft landing,” the end of the rate-hiking cycle in North America appears to be approaching. If so, the economic landscape may alter significantly as we head into the back half of 2023 and into next year.